Buying vs. Renting in the Netherlands: Financial Pros and Cons for Expats

The Financial Pros and Cons for Expats in the Netherlands

Buying vs. Renting in the Netherlands: Financial Pros and Cons for Expats

Navigating the Dutch housing market as an expat means making a crucial decision: should you buy or rent your home? Both paths have significant implications for your finances, lifestyle, and long-term plans. In this guide, we break down the financial pros and cons of each option, helping you make the smartest choice for your unique situation.

The Dutch Housing Market in 2025: A Quick Overview

With historically high demand, limited availability, and rising costs in cities like Amsterdam, Utrecht, and The Hague, both buying and renting have their challenges and opportunities for international residents.

Financial Pros and Cons of Buying a Home

Pros

Builds Equity: Each mortgage payment grows your ownership stake. Over time, you build wealth through property appreciation and by reducing your debt principal.

Stable Monthly Costs: Your mortgage payments remain predictable (especially with a fixed-rate loan), protecting you from sudden rent hikes.

Tax Advantages: Homeowners in the Netherlands benefit from mortgage interest deduction (hypotheekrenteaftrek), significantly reducing your annual tax bill.

Freedom and Customization: Renovate, decorate, or invest in energy efficiency as you wish, no landlord approval needed.

Potential for Long-Term Savings: Over several years, the total cost of owning is often lower than renting comparable properties.

No Capital Gains Tax: When you sell your Dutch home, you typically do not pay capital gains tax.

Cons

Substantial Upfront Costs: Purchase price, transfer tax (unless buying new build), notary fees, mortgage advisor costs, and valuation add up quickly.

Ongoing Expenses: Owners must budget for property taxes, maintenance, repairs, and homeowners’ association fees.

Market Risk: Property values can fluctuate, and selling may take time if the market cools.

Limited Flexibility: Tying up capital in a home reduces mobility, moving for work or personal reasons becomes harder, especially in the short term.

Mortgage Qualification: Not all expats may qualify for a mortgage, and options may be limited by residency, contract type, or credit history.

Financial Pros and Cons of Renting

Pros

Flexibility: Renting allows you to relocate easily, upgrade or downsize as your needs change, and avoid long-term commitments, valuable if your stay in the Netherlands is uncertain.

Lower Upfront Costs: Typically, you only need a security deposit and the first month’s rent.

No Maintenance Costs: The landlord covers most repairs and property taxes, freeing you from surprise expenses.

Tenant Protection Laws: Dutch regulations offer tenant protections that help prevent arbitrary eviction or excessive rent increases (in regulated sectors).

Cons

No Asset Growth: Rent payments build your landlord’s equity, not yours—none of your monthly spend is invested for your future.

Rising Rents: Especially in the free sector, rent prices often rise annually and can drastically outpace inflation, eroding your disposable income.

Limited Choice & Competition: High demand, waitlists, and limited selection make desirable rentals scarce and often expensive.

Unpredictable Landlord Practices: Expats sometimes face poor maintenance, sudden evictions, and deposit issues, especially in major cities.

Fewer Customization Options: Improvements must be approved by the landlord; money spent on upgrades typically benefits them.

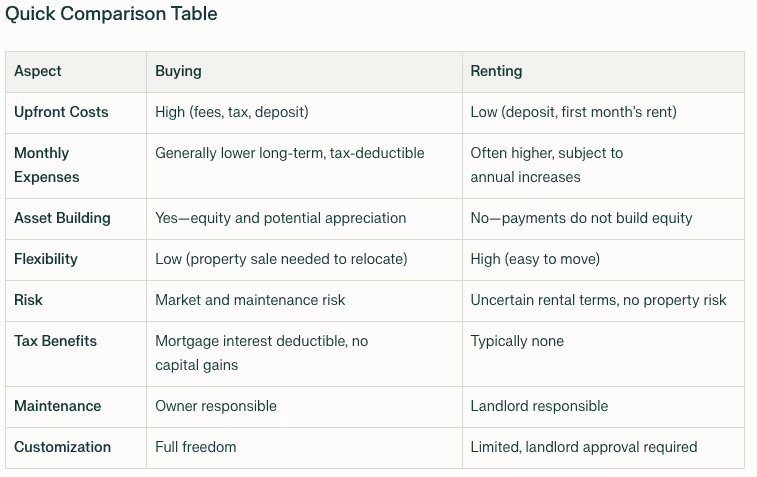

Quick Comparison Table

What Should Expats Consider?

Duration of Stay: If you plan to stay at least 3-5 years, buying often becomes more cost-effective. For shorter stays or uncertain plans, renting provides flexibility.

Job Stability & Residency: Mortgage approval depends on your contract, length of stay, and legal residency.

Market Trends: Consider local price trends, rent levels, and housing availability in your target city.

Upfront vs. Ongoing Costs: Factor all one-time and recurring expenses, not just monthly payments.

The Bottom Line

Both buying and renting have distinctive financial implications for expats in the Netherlands. Understand your personal goals, financial situation, and future plans. If you want to build wealth, enjoy stability, and stay long-term, buying usually makes financial sense. If you value flexibility, have a short-term contract, or are unsure about your future in the Netherlands, renting keeps your options open and your stress lower.

Get Expert Advice: Take The Next Step!

Ready to take the next step? Let Financial Consultancy Holland guide you confidently through every stage of your Dutch homebuying journey. Contact us today for a free consultation and personalized mortgage checklist. With over 200 successful expat mortgage approvals in Amsterdam last year, we know exactly what it takes to help international buyers land a home in the Netherlands.